Apr

When Is Physiotherapy Covered By Insurance In Singapore?

If you’ve recently injured your back, sprained your ankle, undergone surgery or been referred for rehabilitation, one of the first questions that often comes to mind is:

“Will my insurance cover physiotherapy?”

The answer is often yes—but not always.

Unlike a fixed medical fee, insurance coverage for physiotherapy depends on several factors, including your insurance policy, the reason for treatment, the supporting medical documents and sometimes even where you receive treatment.

Understanding these factors before starting treatment can help you avoid unexpected costs and make the claims process much smoother.

In this guide, we’ll explain how physiotherapy insurance works in Singapore, what insurers commonly consider, why some claims are approved while others are declined, and what you can do to improve your chances of a successful claim.

The Short Answer

Many insurance plans in Singapore may provide benefits for physiotherapy when the treatment is considered medically necessary.

However, coverage depends on factors such as:

- Your insurance policy

- The cause of your injury or condition

- Whether referrals or supporting medical documents are required

- The type of benefits included in your plan

- Your policy limits and exclusions

For this reason, two people receiving the same physiotherapy treatment may have very different levels of insurance coverage.

Rather than assuming treatment will be covered, it is always advisable to understand your policy before beginning rehabilitation.

Why There’s No Simple Yes or No Answer

One of the biggest misconceptions is that insurance either “covers physiotherapy” or “doesn’t cover physiotherapy.”

In reality, insurers assess each claim based on the individual circumstances.

For example, a patient recovering from knee surgery may have very different benefits from someone seeking treatment for long-standing neck stiffness.

Similarly, someone receiving physiotherapy after a sports injury may have different coverage from another patient attending physiotherapy for preventive exercise or general wellness.

Insurance is designed primarily to support medically necessary treatment rather than elective or wellness services.

This is why understanding the purpose of your physiotherapy treatment is often just as important as understanding your insurance policy.

What Determines Whether Insurance Covers Physiotherapy?

Several factors influence whether physiotherapy may be claimable.

1. The Type of Insurance You Have

Different insurance plans provide different benefits.

Examples include:

- Integrated Shield Plans (where applicable)

- Employer medical benefits

- Personal accident insurance

- Motor accident insurance

- Work Injury Compensation

- Travel insurance for overseas injuries

Each has its own eligibility requirements, claim procedures and benefit limits.

2. Why You Need Physiotherapy

Insurance providers generally focus on medical necessity.

Treatment following conditions such as:

- Sports injuries

- Ligament tears

- Fractures

- Post-operative rehabilitation

- Shoulder injuries

- Knee injuries

- Neck injuries

- Back injuries

may be viewed differently from treatment requested purely for maintenance or general wellbeing.

The underlying diagnosis often plays an important role during the claims assessment.

3. Your Policy Benefits

Every insurance policy contains its own terms and conditions.

Important areas include:

- Annual claim limits

- Per-treatment limits

- Waiting periods

- Co-payments

- Deductibles

- Excluded conditions

Reading these carefully helps prevent surprises later.

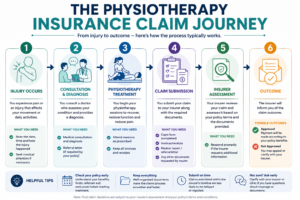

4. Supporting Medical Documentation

Some claims require supporting documents such as:

- Medical reports

- Referral letters

- Imaging reports

- Surgical reports

- Itemised invoices

Incomplete documentation can delay or complicate the claims process.

5. Referral Requirements

Some insurance policies require a doctor’s referral before physiotherapy begins, while others do not.

Because this causes considerable confusion among patients, we’ve written a separate guide explaining referral requirements in detail.

Situations Where Physiotherapy Is Commonly Covered

Although every insurer has different rules, physiotherapy is commonly considered after medical events such as:

Sports Injuries

Examples include:

- Ankle sprains

- Knee ligament injuries

- Tennis elbow

- Rotator cuff injuries

- Muscle tears

The emphasis is often on restoring normal function and returning to daily activities or sport.

Post-Operative Rehabilitation

Physiotherapy frequently forms part of recovery following surgery, including:

- Knee replacement

- Hip replacement

- Shoulder surgery

- ACL reconstruction

- Spinal surgery

Rehabilitation aims to improve mobility, strength and functional recovery.

Accident-Related Injuries

Treatment following:

- Motor vehicle accidents

- Workplace injuries

- Falls

- Fractures

may be claimable under the relevant insurance arrangements, depending on the circumstances and policy terms.

Neurological Rehabilitation

Some patients require physiotherapy following neurological conditions to improve movement, balance and independence.

Coverage depends on the insurance benefits available.

Situations Where Insurance May Not Cover Physiotherapy

Insurance is less likely to cover treatment when it is considered outside the scope of medically necessary rehabilitation.

Examples may include:

- General fitness programmes

- Preventive exercise only

- Wellness treatments

- Maintenance sessions without a medical indication

- Services excluded under the policy

Again, this varies between insurers and policies.

Types of Insurance That May Include Physiotherapy Benefits

Corporate Medical Benefits

Many employers provide outpatient medical benefits that may include physiotherapy.

Coverage varies widely between companies.

Some employers require pre-authorisation or referrals.

Personal Accident Insurance

If an accidental injury results in the need for rehabilitation, physiotherapy benefits may be included depending on the policy.

Motor Accident Insurance

Patients injured in road traffic accidents may be eligible to claim rehabilitation expenses under applicable motor insurance arrangements.

Work Injury Compensation

Employees injured during the course of work may be eligible for treatment benefits under applicable legislation and insurance arrangements.

Travel Insurance

If an injury occurs while travelling overseas, some travel insurance policies may reimburse physiotherapy expenses subject to their terms and conditions.

Why Some Physiotherapy Claims Are Rejected

Claim rejections do not necessarily mean the physiotherapy itself was inappropriate.

Common reasons include:

- The treatment is excluded under the policy.

- The annual benefit limit has been reached.

- Required referrals were not obtained.

- Supporting documents are incomplete.

- Waiting periods still apply.

- The insurer determines the treatment does not meet the policy’s medical criteria.

- The claim was submitted after the deadline.

Understanding these requirements beforehand can save considerable frustration.

How To Improve Your Chances Of A Successful Claim

Although approval is never guaranteed, these practical steps can help.

✔ Understand Your Insurance Policy

Know what benefits your policy provides before starting treatment.

✔ Ask Questions Early

If you’re unsure about referrals, claim procedures or documentation, clarify these before attending your first physiotherapy session.

✔ Keep All Documents

Retain:

- Invoices

- Receipts

- Referral letters

- Medical reports

- Claim forms

These may all be required during the claims process.

✔ Submit Claims Promptly

Many insurers specify claim submission deadlines.

Delaying submission may affect eligibility.

✔ Clarify Benefit Limits

Knowing your available benefits helps you plan treatment more confidently.

Frequently Asked Questions

Is physiotherapy always covered by insurance?

No. Coverage depends on your insurance policy, the medical reason for treatment, policy limits and any applicable claim requirements.

Can I claim physiotherapy without seeing a doctor first?

Some insurance policies allow this, while others require a doctor’s referral. Always check your policy before beginning treatment.

Does MediSave pay for physiotherapy?

MediSave usage depends on the specific healthcare setting, treatment and prevailing regulations. Not all physiotherapy services are MediSave-claimable.

How many physiotherapy sessions will insurance pay for?

There is no universal number. Limits vary between insurance plans and may depend on the condition being treated.

Does employer insurance usually include physiotherapy?

Some employer medical benefits include physiotherapy, while others do not. Coverage varies between organisations.

Is sports physiotherapy covered?

It may be, particularly when treatment is medically necessary following an injury. Coverage depends on your insurance policy.

Does insurance cover physiotherapy after surgery?

Many insurance plans may provide benefits for post-operative rehabilitation, subject to policy terms and conditions.

Final Thoughts

Insurance can make physiotherapy more affordable, but every policy is different.

Rather than assuming treatment will automatically be covered, taking a few minutes to understand your benefits can help you make informed decisions and avoid unnecessary surprises during the claims process.

If you have questions about the documentation required for an insurance claim, the team at BMJ Physiotherapy can help explain the paperwork commonly requested by insurers. Final claim decisions, however, are always subject to your insurer’s assessment and your policy’s terms and conditions.